TechCrunch

The momentum from last year includes 58 startups that raised total funding of €30.39 million, according to a new report just out from long-time Romanian conference How To Web. This represents a 6% increase in the volume of investments overall, and a 51% increase of investments year on year overall. A significant part of these numbers came from companies raising money for the first time.

Key industries include cybersecurity, enterprise software and fintech, with many “super-geeky teams, with deep expertise in the field” as one investor put it. “We are very focused on Romanian founders,” said another. But because of significant emigration in recent years, “they can reside and launch anywhere in the world.”

Here are the investors in their own words, for any TechCrunch reader who is interested in hiring, investing or founding a company in the country:

- Cristian Negrutiu, Founding Partner, Sparking Capital

- Cristian Munteanu, Managing partner, Early Game Ventures

- Andrei Pitis, Founding Partner, Simple Capital

- Bogdan Axinia, Managing Partner, eMAG Ventures

- Dan Mihaescu, Founding Partner, GapMinder Ventures

- Alexandru Popescu, Managing Partner, Cleverage Venture Capital

- Theodor Genoiu, Associate, Roca X

- Matei Dumitrescu, Founding Partner, Impact Capital

Oh, and one more thing. We just launched Extra Crunch in Romania. Subscribe to access all of our investor surveys, company profiles and other inside tech coverage for startups everywhere. Save 25% off a one- or two-year Extra Crunch membership by entering this discount code: ECROMANIA

Cristian Negrutiu, Sparking Capital, Founding Partner

What trends are you most excited about investing in, generally?

Given the incipient stage of Romanian ecosystem, our fund is industry agnostic. On a personal note, I’m interested in verticals like supply chain, mobility, proptech, circular/sharing economy.

What’s your latest, most exciting investment?

Our latest investment is a start-up in the digital fitness industry.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

I would like to see more solutions in supply chain, as I believed that this industry needs a paradigm shift.

What are you looking for in your next investment, in general?

1. Relevant market 2. Good product 3. Excellent team 4. Fit with us

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

I believe that in marketing and finance is difficult to enter or you need something really different. In terms of products/services, marketplaces need to evolve in order to be competitive

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We are strongly focused on Romania

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Romanian ecosystem is still in infancy, but with a high velocity and very good prospects for the future. I believe that we will see soon more Romanian unicorns, including from our portfolio

How should investors in other cities think about the overall investment climate and opportunities in your city?

As said above – still in early stages, but full of opportunities and going full speed

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Not for Romania. The ecosystem is still based on few cities like Bucharest, Cluj, Iasi and the hubs within those cities

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Apart from traditional HoReCa (Hotel/Restaurant/Café) businesses and overall trends, we didn’t see much impact. Actually, any start-up that promotes digitization in a specific industry (e.g. proptech) gained momentum in this period.

How has COVID-19 impacted your investment strategy?

We tried to be as normal as possible and maintain a steady flow of business. We advise founders to look after their teams and customers and be careful with cash

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes, as mentioned above.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

We always need to be positive and not exaggerate about the pandemic. It will pass.

Cristian Munteanu, Managing partner, Early Game Ventures

What trends are you most excited about investing in, generally?

Given our limited geographical scope (we invest only in Romania), we have to have a generic approach and consider many verticals and trends. Just as an example, we are looking at startups applying technologies that reached mass adoption to niche fields: computer vision applied to specific crops (agritech) or applied to in-store customer behaviour (martech); biometric data (collected through wearable devices) applied to group interactions as opposed to single individuals; ultra-light blockchain ledgers applied to smart buildings… From another investment perspective, we are looking to invest in what we call “the infrastructure for innovation” such as startups building APIs — we believe that Romania is not yet API-fied enough.

What’s your latest, most exciting investment?

The last term sheet we signed was with a startup that is building technology to help enterprise-level companies to better manage their software licenses. Super-geeky team, with deep expertise in the field, creating a lot of value to their customers.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

I would like to find great teams trying to make in-game payments easier (building at the intersection of payments and gaming), or working on Irrigation-as-a-Service (agritech), or building a NASDAQ for energy.

What are you looking for in your next investment, in general?

I am looking for founders that are both super competent and brave. Such people will dare tackle big problems and will have a chance to succeed at solving it.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

I’ve seen too many startups building apps to help people find parking spots, too many marketplaces that no one need, too much off the shelf technology for marketing, too many CRMs and ERPs.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We are investing only in Romania — 100% committed to the local ecosystem.

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

I think that, given the natural potential of Romania, agritech has a big chance; still this space is not fully serviced yet. Otherwise, cybersecurity, enterprise software, and fintech are quite well represented. From our portfolio of almost 20 startups, CODA is enabling managed service providers with cybersecurity skills; Humans is building a hub for synthetic media technologies; Mechine is making agricultural equipment speak to each other; Tokinomo is collecting and analyzing data from the shelf (in-store marketing); BunnyShell is building next-gen cloud tech and making it easy for anyone to set up servers in three clicks.

How should investors in other cities think about the overall investment climate and opportunities in your city?

The startup ecosystem in Romania is very young, with the first local VC funds established three years ago with support from the European Investment Fund. And yet, Romania is home to three unicorns and many other promising startups. The large technical talent pool, the widely spread broadband access and the low costs of doing business and living turn Romania into a market to keep an eye on.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

I expect founders from the big cities to stay in the big cities as setting up and working for a startup does not mean writing code on the laptop from a remote beach. In the tormenting search for product-market fit, founders need to talk business, visit partners, sign contracts, attend events, meet peers, do surveys, prototype and one thousand other things that cannot be done on Zoom to their full extent. The tech industry and the startupland took a hit from the pandemic as the rest of the world. And just as the rest of the world, they will survive, adapt, and mostly return to the normal interactions from before March 2020.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Unfortunately, I saw urban mobility apps suffer from the restrictions imposed by the pandemic. Also, anything related to restaurants, hotels and conventional events was badly affected. We are invested in startups in these verticals and made everything we could to help them during the worst days of the pandemic.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Our fund registered a 20% decrease in the numbers of investments in 2020 compared to 2019 and a 40% decrease in the total value of deals; so the impact of COVID was significant. At the same time, in terms of fund performance, 2020 was a good year, with companies in our portfolio raising new investment rounds with outside investors, increasing their valuation, and showing good returns. The first half of 2020 was dedicated to damage control measures and supporting the portfolio companies, but the situation changed towards the end of the year, with high new deals activity in the last quarter (higher than in Q4 2019). VC-backed startups had investors to turn to in harsh times and benefited from support and additional funds when needed; things were much more difficult for the rest of the startups though.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Probably the first thing we noticed the moment the pandemic started was a peak in productivity. During the months of mandatory shelter at home, the early-stage startups working on their prototypes put in extra-hours and gained speed. Personnel retention was good, people were focused, there was a positive spirit and a general desire to make things happen. Indeed, some startups reported an immediate boost of sales, such as Tokinomo whose robots replace the human promoters in supermarkets.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

The highlight of 2020 was the week I spent on a magnificent yacht sailing with friends through the islands in Greece. It was a recharging moment that gave me a boost for the rest of the year. The next elating moment came in December with the Series A investments that increased our fund’s performance.

Andrei Pitis, Founding partner, Simple Capital

What trends are you most excited about investing in, generally?

Startups creating world leading Intellectual Property with Romanian and broader Eastern European founders

What’s your latest, most exciting investment?

Uniapply.com

What are you looking for in your next investment, in general?

Strong committed founders with deep understanding of the domain they are planning to disrupt on a global scale through innovative intellectual property.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

I think too many people are trying to launch platforms without much understanding of how hard it is to launch it in the absence of a major differentiator. Customer acquisition through other digital marketing platforms is very expensive if there is no other unfair advantage to launch such a platform.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We are very focused on Romanian founders — but they can reside and launch anywhere in the world. We have investments in many US-based companies started by Romanian founders.

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

I think Romania is very well positioned to win in cybersecurity and enterprise software as well as AI-based engines. I am very excited about pentest-tools.com, deepstash.com, uniapply.com from our portfolio as well as Fintech OS and TypingDNA that are not in our portfolio.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Bucharest is a thriving ecosystem with plenty of opportunities ripe for global expansion.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Indeed we have seen a surge in founders from smaller cities in Romania. We are founding partners of the Innovation Labs pre-accelerator that has a nationwide footprint and we are seeing more and more students interested in becoming founders all over Romania.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Mobility solutions are impacted, local players are losing to bigger players like Lime.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

The pandemics delayed a lot of the investments, but we closed them toward the end of the year. Biggest worries for founders is that they have less and less leverage as a startup to attract tech talent. The problem is that the tech people can now work for any company in the world and this skyrocketed their salaries/rates.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes we have seen — some of them benefited from people staying at home and having more time.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

The introduction of the vaccine and the pace at which people are vaccinated in Romania, that is not the fastest but also not the slowest either. An online platform for appointments is up and running and people are using it!

Bogdan Axinia, Managing partner, eMAG Ventures

What trends are you most excited about investing in, generally?

Health & wellbeing are areas that “helped” by the pandemic crisis are on brink of transformation and growth. A blend of software and hardware readiness is developing fast together with the openness of clients and regulatory authorities.

What’s your latest, most exciting investment?

Food delivery services. It is still day 0 with great opportunities ahead in terms of consumer services and business growth: food, ready to cook meals, convenience items, grocery, etc.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

It is still room to grow on B2C and B2B2C fintech space despite relatively high numbers of startups.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

Bucharest and Romania in general have great potential when we look at talent pool from tech perspective and are a great place to start to scale regional and globally.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Great place to come: great infrastructure (internet cost & speed, number of hubs), talent pool and increased number of investments transactions in last 3 years.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

I expect to see a growth but not a surge of founders from other geographies. And I believe thats a good thing for the ecosystem.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Travel is both exposed and in the same time with great potential for new startups to come. There will be a “revenge travel” period from consumers but they will look for something different and in the same time business travel will not be the same and this will generate new practices and behaviour.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

We see opportunities to grow and we are allocating more capital for investments and we are advising our startups to invest more and grow faster.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

The start of the vaccine campaign across the globe and the initial results.

Dan Mihaescu, Founding partner, GapMinder Ventures

What trends are you most excited about investing in, generally?

B2B platforms enabled by ML/automation/AI in fintech, SaaS enterprise software, cybersecurity, healthcare IT, low-code development environments, conversational technologies, automation in logistics

What’s your latest, most exciting investment?

– Latest investment was DruidAI, announced on January 12th, 2021. GapMinder led a $2.5M round.

– Other 2020 exciting new investments or follow-ons: TypingDNA, FintechOS, DeepStash, Soleadify, Machinations, Innoship, Frisbo, Cartloop, XVision

What are you looking for in your next investment, in general?

– Stage: Seed or Series A

– Technology: Automation or conversational technology assisted by ML or AI

– Team: Mature with track-record for International expansion;

– Product: B2B scalable international, with B2B platforms as main focus

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

Copies of B2C models (from US) that are borne in CEE tend to be limited to small local markets, and evolve into highly crowded environments. Shared economy companies borne in Romania are such examples. Unit economics were simply not attractive for us as VC investor.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

More than 70%

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

– Models we consider will continue to thrive: B2B platforms enabled by automation/conversational technologies (assisted by ML/AI) have a higher potential for internationalisation vs B2C models.

– Reg verticals with higher potential, we mentioned above a few.

– GapMinder portfolio exciting companies: FintechOS, TypingDNA, DeepStash, DruidAI, Soleadify, Machinations, Innoship, Frisbo, Cartloop, SmartDreamers, XVision, among others

How should investors in other cities think about the overall investment climate and opportunities in your city?

Romania (in cities such as Bucharest, Cluj, Timisoara, Brasov, Oradea and Iasi) is a high-opportunity market, with excellent teams, startups borne with international vision, excellent environment for automation and ML enabled projects.

The ecosystem becomes more mature, from coverage of pre-seed rounds towards Series A, while not overcrowded yet.

Overall, a high opportunity environment for Series B and late Series A investors from US or rest of Europe.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

The hubs are concentrated in terms of education pool, potential customers (B2B or more sophisticated B2C) to test new products, potential investors on the pre-seed phase that are crucial for the initial steps of start-up developments.

For more advanced start-ups, hyper-growth is important, therefore the capability to scale up and go international might be helped by the presence in certain hubs.

In other words, there is a complex mix that the hubs are offering. So, at Romanian level, we do not expect a diminishing role of the hubs.

At European or US level, it is debatable if main hubs are too overcrowded or over-expensive for the teams. However, the business growth potential for the more advanced start-ups is important.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

The behaviour of users, both internal and external, has migrated towards a need for autonomy, which drives the need for:

– Tools that allow conversational interactions (including in natural language) with evolved human like feeling

– Remote collaborative low code development tools

– A general need for all companies (from the smallest ones to enterprise) to move yesterday to digital interactions

In 2020 a lot of consumers and companies were forced to focus on core priorities, and move to secondary focus the “nice-to-have” services or products. The VCs have seen even a sharper delimitation between high-tech and tech-enabled companies, not to mention some “interesting” proofs of Fake Tech. This shift has impacted lots of verticals, and such shift might be here to stay.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

GapMinder’s strategy described above is focussed on companies that actually have been benefiting from the tide of urgency in accelerating digital transformations of companies. And we seen it in the 2x-3x growth of most of our portfolio companies in 2020.

Our advices to our portfolio companies have been simple:

1. Cash is king. Make sure you have an 18 months minimum runway. If an opportunity to raise, seriously consider it.

2. Customers are the most important partners you have. Listen to them

3. The team is your most important asset. Keep it close and take care of it in these daring times.

4. Act fast

Of course, on top of the above, we had very specific conversations with each team.

To be candid, this all looks good at the end of 2020, but the first half of 2020 has been intense for founders in our portfolio and filled with doubts about decisional freeze in some verticals, stress on implementation in international markets wherever travel was needed, alignment between teams inside larger companies. Looking back, this was just normal. We feel fortunate to be part of the life of such great teams and start-ups, that proved so good during tough times.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes, we already felt signs of recovery in second half of 2020, especially Q4.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Starting at scale the vaccination against COVID-19 in last 6 weeks is definitely the most important positive sign at human level, society level, but also from a pure business perspective.

In our team, GapMinder, we feel optimistic!

Alexandru Popescu, Managing Partner, Cleverage Investment

What trends are you most excited about investing in, generally?

HealthTech

What’s your latest, most exciting investment?

Oncochain

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

What are you looking for in your next investment, in general?

Team, idea, traction

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

50%

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Sanopass; Oncochain ( our portfolio); Fintech ( Fintech OS – Teodeor Blidarus; Sergiu Negut)

How should investors in other cities think about the overall investment climate and opportunities in your city?

Very dynamic yet at an early stage

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

No.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Telemedicine – advantage; dentistry – exposed;

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

No impact due COVID; biggest worries are related to teams maturity & to market capacity to absorb new ideas fast enough; my advice is to look for know-how and try to grow as fast as possible

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Definitely I see “green shoots”

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Much better evaluation of one of our investments after only few months

Theodor Genoiu, Associate, Roca X

What trends are you most excited about investing in, generally?

Edutech, energy, deeptech

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

eCommerce marketplaces, some service areas, mobility

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

Our thesis has a goal of a 40% distribution of the AuM in Romania

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Positive industry outlook – edutech, medtech, fintech, logistics;

Exciting companies – Fintech OS, Medicai, Kinderpedia, iFactor and a few others.

Negative industry outlook – marketplaces, Deeptech, gaming (in terms of funding, not talent), advertising

How should investors in other cities think about the overall investment climate and opportunities in your city?

Growing ecosystem with a large technical talent pool but in need of true entrepreneurial education, experience and mentality.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Yes and no, in more established ecosystems a surge in founders coming from geographies outside major cities might be an outcome, the onset of remote work will bring a major boost to startups, although talented technical employees will become more and more difficult to onboard.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Our investment strategy remains unchanged, the most commons worries of founders in our portfolio are linked to attracting new funding partners, lack of foresight in some target markets and difficulty in finding employees in certain verticals. We don’t have a general advice for all our startups, it’s case by case, we advise some to pivot, others to start conversion efforts on their large customer base and others to launch in new geographies.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

The openness to adopt new technologies and try new things from well-known conservative verticals such as education.

Matei Dumitrescu, Founding Partner, Smart Impact Capital

What trends are you most excited about investing in, generally?

Impact, health, energy

What’s your latest, most exciting investment?

iFactor, Ringhel, Sanopass

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

Yes, there are: impact startups

What are you looking for in your next investment, in general?

Impact, innovation, scalability

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

Marcom, ecomm, marketplaces

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

Almost 100% focused on local startups with a global view

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Tech, ehealth. Medicai and its founder Mircea Popa are examples of great potential.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Bucharest is booming, the market in getting bigger, the VCs are growing, the number of new initiatives is dramatically increased.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

No, but remote work is possible

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

We had an opportunity with e-education and e-health. However, sharing economy was exposed to problems.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Our startups were already agile, working remote and selling through digital channels digital products or services.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes, we do.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

There wasn’t such moment.

Any other thoughts you want to share with TechCrunch readers?

We invest in IMPACT, because the impact creates VALUE, and that is what people pay for!

]]>

TechCrunch

At the time, seven-figure seed investments in African startups were a rarity. But over the years, those same seed-stage rounds have become more common, with some very early-stage startups even raising eight-figure sums. Nigerian fintech startup, Kuda, which bagged $10 million last year, comes to mind, for example.

Also notable amidst the growth in seven and eight-figure African seed deals have been gains in pre-seed fundraising. Typically, pre-seed rounds are raised when the startup is still in the product development phase, yet to make revenue or discover product-market fit. These investments are usually made by third-party investors (friends and family), and range between $25,000-$150,000.

But the narrative as to how much an early-stage African startup can raise as pre-seed has changed.

Last year, African VCs who usually fund seed and Series A rounds began partaking in pre-seed rounds, and they don’t seem to be slowing down. Just a month into 2021, Egyptian fintech startup Cassbana raised a $1 million pre-seed investment led by VC firm Disruptech in a bid to drive expansion within the country.

So why the sudden change in appetite from investors?

Andreata Muforo is a partner at TLcom Capital, a pan-African early-stage VC firm. She told TechCrunch that last year’s run of 23 pre-seed rounds (10 of which were $150,000+ deals) per Briter Bridges data, was due to the confidence investors had in the market, especially fintech.

Startups building financial infrastructure got noticed

While most African pre-seed investments in 2020 went to fintech, there were exceptions, including Egyptian edtech startup Zedny, which raised $1.2 million; Nigerian automotive tech startup Autochek Africa, which raised $3.4 million; and Nigerian talent startup TalentQL, which raised $300,000.

Just as Paystack and Flutterwave built payment infrastructure for thousands of African businesses, these fintech startups are trying to make their mark in the sweet spots of credit and banking.

“Fintech is compelling. But while most fintech startups play around the commodities side of fintech, it’s the companies building infrastructure around the market that got most of the pre-seed validation last year,” Muforo said. Her firm, TLcom, led the $1 million pre-seed investment in Okra.

Okra is an API fintech startup. So are Mono, OnePipe and Pngme. They are building Africa’s API infrastructure that connects bank accounts with financial institutions and third-party companies for different purposes. Within the past 18 months, Mono and Pngme raised $500,000, while OnePipe raised $950,000 in pre-seed.

It is noteworthy that while these startups are clamoring to solve Africa’s open API banking issues, three of the four deals came after Visa’s $5.3 billion acquisition of Plaid last year in January.

Although the Visa-Plaid acquisition has now been called off, it is safe to say some African investors developed FOMO, handing out sizable checks to fund “Africa’s Plaid” in the process.

Digital lenders remain one of their most important customers for fintech API startups. They can access customers’ financial accounts to understand their spending patterns and know who to loan to.

Egypt’s Shahry and Nigeria’s Evolve Credit are fintech startups building credit infrastructure for their markets. Evolve Credit connects digital lenders to those who need loan services in Nigeria via its online loan marketplace. Shahry, on the other hand, employs an AI-based credit scoring engine so users in Egypt can apply for credit. The pair also secured impressive pre-seed funding — Evolve Credit, $325,000, and Shahry, $650,000.

A recurring theme: Serial founders

Muforo points out that aside from startups building fintech infrastructure, the caliber of founders was another reason pre-seed funding peaked last year.

Adewale Yusuf, co-founder and CEO of TalentQL, a startup that hires, manages and outsources talent for Nigerian and global companies, seemed to agree. He told TechCrunch that trust between the VCs and founders involved played a major role in most pre-seed rounds last year.

“It wasn’t surprising that a lot of investors put money in pre-seed rounds. I say this because we also saw existing founders and serial entrepreneurs coming back to the market. To me, these founders’ credibility was a major part of why those rounds were large,” he said.

A second-time founder himself, Yusuf is the co-founder of Nigerian tech media publication Techpoint Africa. His partner at TalentQL, Opeyemi Awoyemi, is also a serial entrepreneur. He co-founded Ringier One Africa Media-owned Jobberman, one of Africa’s most popular recruitment platforms.

According to Adedayo Amzat, founder of Zedcrest Capital, which is the lead investor in TalentQL’s round, the founders’ experience proved vital in closing the deal.

He says investors are more comfortable backing experienced founders in pre-seed rounds because they have a more mature understanding of the problems they’re trying to solve. So, in essence, they tend to raise more capital.

“If you look at pre-seed sizes, experienced founders can demand a significant premium over first-time founders,” Amzat said. “Pre-seed valuation cap for first-time founders will typically be between 400K to $1 million while we frequently see up to $5 million for experienced founders.”

It was a recurring theme last year. Yele Bademosi, who runs Microtraction, a West African early-stage VC firm, is the CEO of Bundle Africa, a Nigerian-based crypto-exchange startup that raised $450,000 in April 2020.

Shahry co-founders Sherif ElRakabawy and Mohamed Ewis also run Egypt’s largest shopping engine and price comparison website, Yaoota.

Mono co-founder and CEO Abdulhamid Hassan was the co-founder of Nigerian fintech startup OyaPay and data science startup Voyance. Also, Etop Ikpe, the co-founder and CEO of Autochek Africa, was CEO of DealDey and Cars45.

That said, Fara Ashiru Jituboh of Okra and Akan Nelson of Evolve Credit as first-time founders got investments that most of their counterparts would only dream of. For Jituboh, her solid tech background spoke for her — boasting a senior software engineering job at Pexels and engineering consultant role at Canva before founding Okra.

“We backed Fara because she’s a strong tech founder. When you look at the core of what Okra does as a tech-heavy company, you see how important it was to make the decision,” Muforo said about backing Okra’s CEO and CTO.

Nelson also told TechCrunch that his finance background helped Evolve Credit raise its six-figure sum. The team’s bullishness on finding product-market fit and the potential of Africa’s loan marketplace was also enough to bring foreign and local VCs like Samurai Incubate, Future Africa, Ingressive Capital and Microtraction on board.

While early-stage investments in African startups haven’t reached full speed, the explosion in the number of angel investors has lowered entry barriers into early-stage investing.

Now investors are beginning to show readiness toward African startups that have promise as they continue to search for the next Paystack.

“More people are willing to take risks now in the market, especially angel investors. They can easily let go of $10K-$50K because of success stories like Paystack,” Yusuf said about the $200 million acquisition by U.S. payments startup Stripe.

For all of its significance to the African tech ecosystem, what particularly stands out about Paystack’s exit is the return on investment made for early investors.

By the time it exited in October 2020, some angel investors had an ROI of more than 1,400% according to Jason Njoku in his blog post. Njoku, who took part in the round as an angel investor, is the CEO of IROKO, a Nigerian VOD internet company.

For Muforo, witnessing more early-stage investments is a big deal, one the African tech ecosystem should savor regardless of the round in question.

“Pre-seed or seed are just names investors and founders give,” she said. “What I think is most important is the fact that we’re getting more early-stage capital into Africa, and startups are getting more attention from investors, which is fantastic.”

]]>

TechCrunch

The complaint, which has been filed by six MEPs and is being supported by the privacy campaign group noyb, alleges third-party trackers were dropped without proper consent and that cookie banners presented to visitors were confusing and deceptively designed.

It also alleges personal data was transferred to the U.S. without a valid legal basis, making reference to a landmark legal ruling by Europe’s top court last summer (aka Schrems II).

The European Data Protection Supervisor (EDPS), which oversees EU institutions’ compliance with data rules, confirmed receipt of the complaint and said it has begun investigating.

It also said the “litigious cookies” had been disabled following the complaints, adding that the parliament told it no user data had in fact been transferred outside the EU.

“A complaint was indeed filed by some MEPs about the European Parliament’s coronavirus testing website; the EDPS has started investigating it in accordance with Article 57(1)(e) EUDPR (GDPR for EU institutions),” an EDPS spokesman told TechCrunch. “Following this complaint, the Data Protection Office of the European Parliament informed the EDPS that the litigious cookies were now disabled on the website and confirmed that no user data was sent to outside the European Union.”

“The EDPS is currently assessing this website to ensure compliance with EUDPR requirements. EDPS findings will be communicated to the controller and complainants in due course,” it added.

MEP, Alexandra Geese, of Germany’s Greens, filed an initial complaint with the EDPS on behalf of other parliamentarians.

Two of the MEPs that have joined the complaint and are making their names public are Patrick Breyer and Mikuláš Peksa — both members of the Pirate Party, in Germany and the Czech Republic respectively.

We’ve reached out to the European Parliament and the company it used to supply the testing website for comment.

The complaint is noteworthy for a couple of reasons. Firstly because the allegations of a failure to uphold regional data protection rules look pretty embarrassing for an EU institution. Data protection may also feel especially important for “politically exposed persons like Members and staff of the European Parliament”, as noyb puts it.

Back in 2019 the European Parliament was also sanctioned by the EDPS over use of a U.S.-based digital campaign company, NationBuilder, to process citizens’ voter data ahead of the spring elections — in the regulator’s first-ever such enforcement of an EU institution.

So it’s not the first time the parliament has gotten in hot water over its attention to detail vis-à-vis third-party data processors (the parliament’s COVID-19 test registration website is being provided by a German company called Ecolog Deutschland GmbH). Once may be an oversight, twice starts to look sloppy…

Secondly, the complaint could offer a relatively quick route for a referral to the EU’s top court, the CJEU, to further clarify interpretation of Schrems II — a ruling that has implications for thousands of businesses involved in transferring personal data out of the EU — should there be a follow-on challenge to a decision by the EDPS.

“The decisions of the EDPS can be directly challenged before the Court of Justice of the EU,” noyb notes in a press release. “This means that the appeal can be brought directly to the highest court of the EU, in charge of the uniform interpretation of EU law. This is especially interesting as noyb is working on multiple other cases raising similar issues before national DPAs.”

Guidance for businesses involved in transferring data out of the EU who are trying to understand how to (or often whether they can) be compliant with data protection law, post-Schrems II, is so far limited to what EU regulators have put out.

Further interpretation by the CJEU could bring more clarifying light — and, indeed, less wiggle room for processors wanting to keep schlepping Europeans’ data over the pond legally, depending on how the cookie crumbles (if you’ll pardon the pun).

Additionally, noyb notes that the complaint asks the EDPS to prohibit transfers that violate EU law.

“Public authorities, and in particular the EU institutions, have to lead by example to comply with the law,” said Max Schrems, honorary chairman of noyb, in a statement. “This is also true when it comes to transfers of data outside of the EU. By using US providers, the European Parliament enabled the NSA to access data of its staff and its members.”

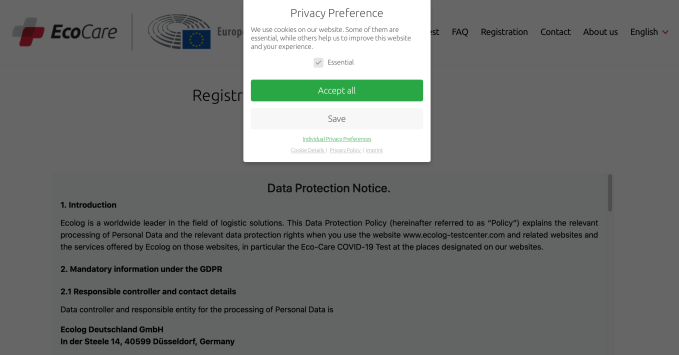

Per the complaint, concerns about third-party trackers and data transfers were initially raised to the parliament last October — after an MEP used a tracker-scanning tool to analyze the COVID-19 test-booking website and found a total of 150 third-party requests and a cookie were placed on her browser.

Specifically, the EcoCare COVID-19 testing-registration website was found to drop a cookie from the U.S.-based company Stripe, as well as including many more third-party requests from Google and Stripe.

The complaint also notes that a data protection notice on the site informed users that data on their usage generated by the use of Google Analytics is “transmitted to and stored on a Google server in the US”.

Where consent was concerned, the site was found to serve users with two different conflicting data protection notices — with one containing a (presumably copy/pasted) reference to Brussels Airport.

Different consent flows were also presented, depending on the user’s region, with some visitors being offered no clear opt-out button. The cookie notices were also found to contain a “dark pattern” nudge toward a bright green button to “Accept all” processing, as well as confusing wording for unclear alternatives.

A screengrab of the cookie consent prompt that the parliament’s COVID-19 test-booking website displayed at the time of writing — with still no clearly apparent opt-out for non-essential cookies (Image credit: TechCrunch)

The EU has stringent requirements for (legally) gathering consents for (non-essential) cookies and other third-party tracking technologies, which states that consent must be clearly informed, specific and freely given.

In 2019, Europe’s top court further confirmed that consent must be obtained prior to dropping non-essential trackers. (Health-related data also generally carries a higher consent-bar to process legally in the EU, although in this case the personal information relates to appointment registrations rather than special category medical data.)

The complaints allege that EU cookie consent requirements are not being met on the website.

While the presence of requests for U.S.-based services (and the reference to storing data in the U.S.) is a legal problem in light of the Schrems II judgement.

The U.S. no longer enjoys legally frictionless flows of personal data out of the EU after the CJEU torpedoed the adequacy arrangement the Commission had granted (invalidating the EU-U.S. Privacy Shield mechanism) — which in turn means transfers of data on EU peoples to U.S.-based companies are complicated.

Data controllers are responsible for assessing each such proposed transfer, on a case by case basis. A data transfer mechanism called Standard Contractual Clauses was not invalidated by the CJEU. But the court made it clear SCCs can only be used for transfers to third countries where data protection is essentially equivalent to the legal regime offered in the EU — doing so at the same time as saying the U.S. does not meet that standard.

Guidance from the European Data Protection Board in the wake of the ruling suggests that some EU-U.S. data transfers may be possible to carry in compliance with European law. Such as those that involve encrypted data with no access by the receiving U.S.-based entity.

However, the bar for compliance varies depending on the specific context and case.

Additionally, for a subset of companies that are definitely subject to U.S. surveillance law (such as Google) the compliance bar may be impossibly high — as surveillance law is the main legal sticking point for EU-U.S. transfers.

So, once again, it’s not a good look for the parliament website to have had a notice on its COVID-19 testing website that said personal data would be transferred to a Google server in the U.S. (Even if that functionality had not been activated, as seems to have been claimed.)

Another reason the complaint against the European Parliament is noteworthy is that it further highlights how much web infrastructure in use within Europe could be risking legal sanction for failing to comply with regional data protection rules. If the European Parliament can’t get it right, who is?

Indeed, noyb filed a raft of complaints against EU websites last year, which it had identified still sending data to the U.S. via Google Analytics and/or Facebook Connect integrations a short while after the Schrems II ruling. (Those complaints are being looked into by DPAs across the EU.)

Facebook’s EU data transfers are also very much on the hook here. Earlier this month the tech giant’s lead EU data regulator agreed to “swiftly resolve” a long-standing complaint over its transfers.

Schrems filed that complaint all the way back in 2013. He told us he expects the case to be resolved this year, likely within around six to nine months. So a final decision should come in 2021.

He has previously suggested the only way for Facebook to fix the data transfers issue is to federate its service, storing European users’ data locally. While last year the tech giant was forced to deny it would shut its service in Europe if its lead EU regulator followed through on enforcing a preliminary order to suspend transfers (which it blocked by applying for a judicial review of the Irish DPC’s processes).

The alternative outcome Facebook has been lobbying for is some kind of a political resolution to the legal uncertainty clouding EU-U.S. data transfers. However the European Commission has warned there’s no quick fix — and reform of U.S. surveillance law is needed.

So with options for continued icing of EU data protection enforcement against U.S. tech giants melting fast in the face of bar-setting CJEU rulings and ongoing strategic litigation like this latest noyb-supported complaint, pressure is only going to keep building for pro-privacy reform of U.S. surveillance law. Not that Facebook has openly come out in support of reforming FISA yet.

]]>